The current surge in the US housing market shows little indication of slowing down any time soon; figures for Q2 of 2021 show record increases in a number of sales as well as prices of homes sold. Prices continue to rise this year, twice as fast as original predictions. In fact, house prices are forecast to outpace the growth of both GDP and domestic inflation.

Factors driving this growth include:

- Low inventory combined with high demand

- A strong economic recovery from the pandemic, with huge fiscal support from government

- Ultra-low interest rates

- Increased demand for extra living space resulting from the work-from-home movement

Record increases by the numbers:

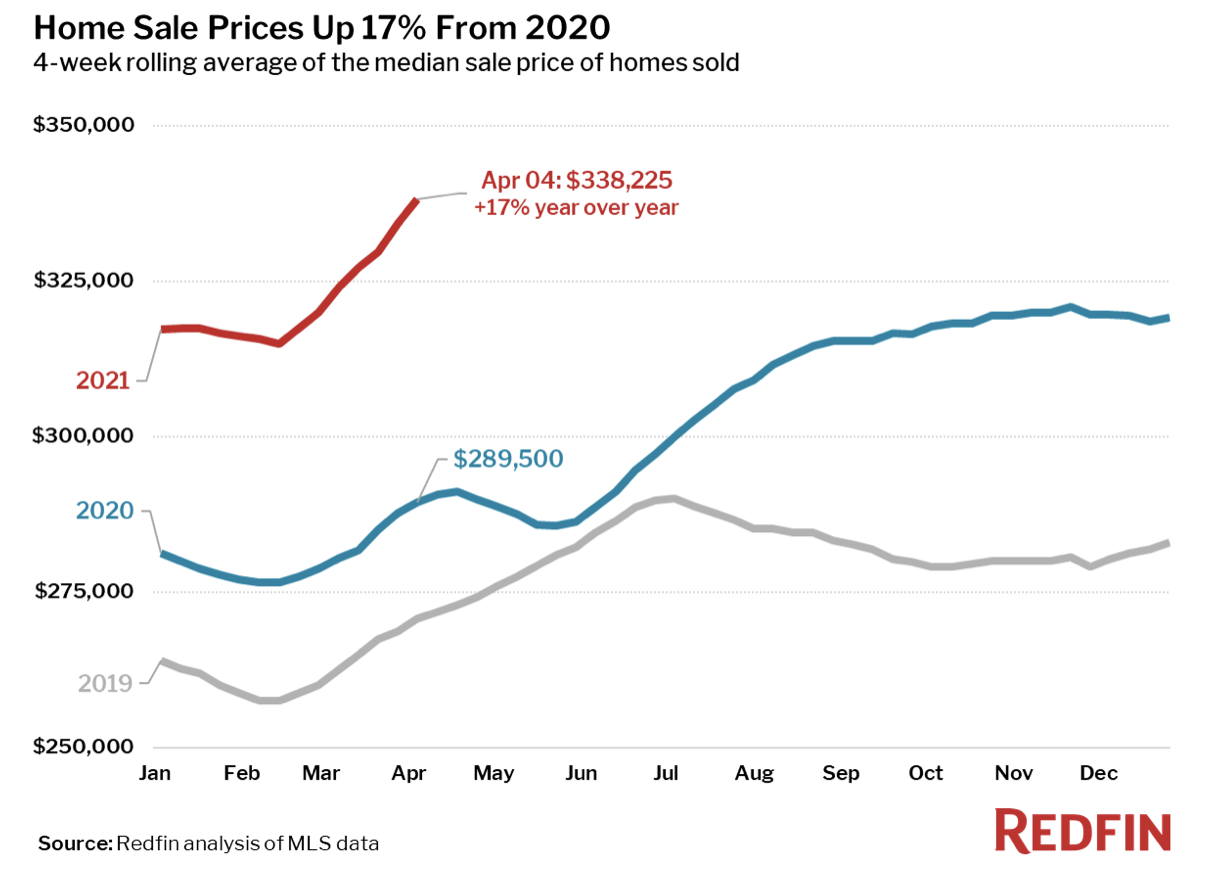

- Median home-sale price increased by record-breaking 17 percent year over year since 2020 (now $388,225)

- Listing prices jumped 16 percent year over year (now $351,851)

- Pending sales up 47 percent on 2020

- Drop in active listings of 42 percent from 2020 – an all-time low

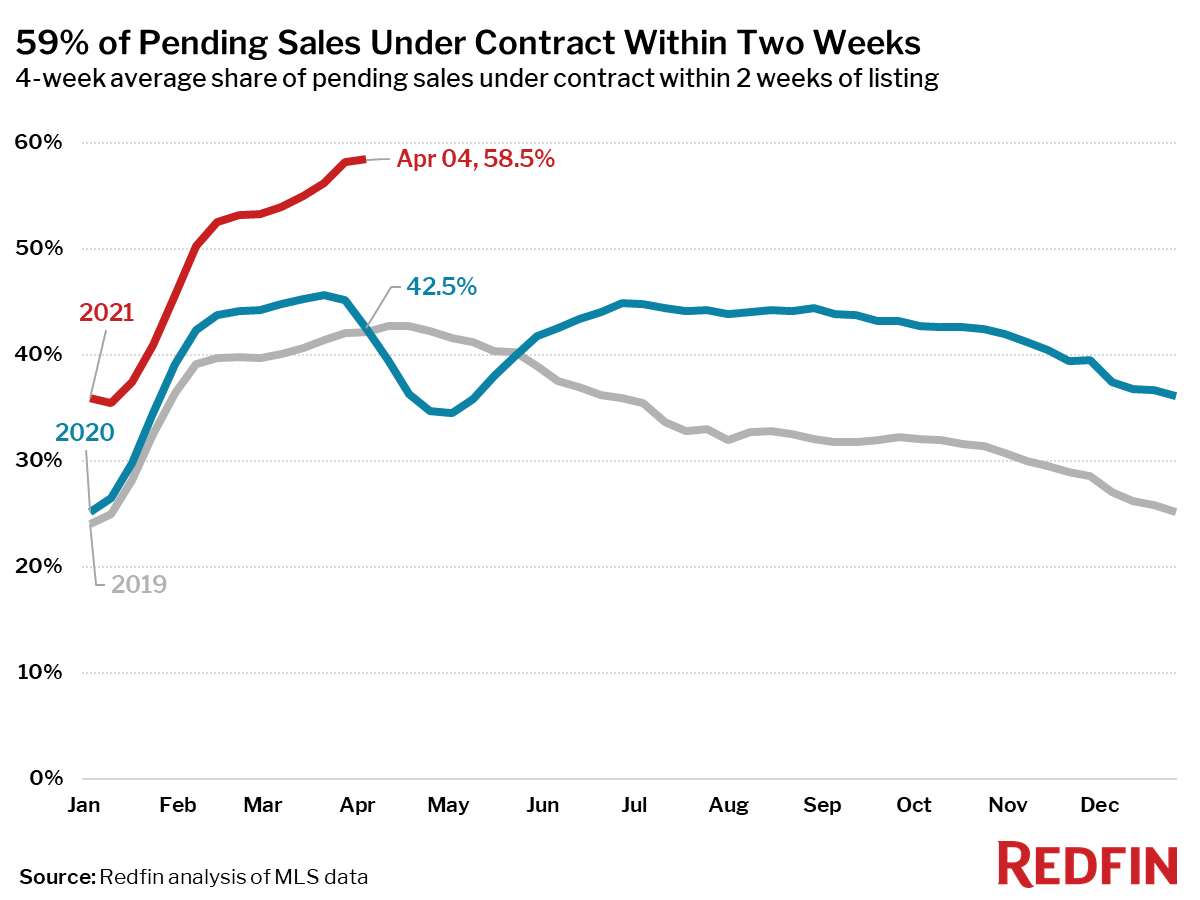

- Almost 60 percent of homes on the market received an accepted offer within two weeks – another record

- $1.2 trillion in equity (average $26,000 per house) added to the US real estate market due to price appreciation

Can this situation continue, or is the market nearing a peak?

Hari Kishan, writing for Reuters.com, predicts that prices will continue to race ahead with risks skewing to the upside. Kishan does not foresee an imminent bubble as fiscal assistance from the government is helping mortgaged owners, as are the current low-interest rates; however, responders to a Reuters poll do foresee some cooling down to more moderate price rises in 2023, following anticipated seasonal changes in fall and winter.

Meanwhile, Prashant Gopal, writing for Bloomberg.com, talks of a “buying frenzy” as Americans utilize ultra-low mortgage interest rates to finance homes in suburbs and more affordable parts of the country – often triggering bidding wars. Gopal cites the picturesque town of Kingston, NY, about 90 miles south of Manhattan, as showing the largest increase in property prices nationwide with a massive 35.5 percent increase over 2020. This frenzy may be fueled by a desperate fear of missing out, as the gap between income and house prices rises at a rate of knots, but there are few indications that the market has peaked.

The combination of low inventory and increased demand obviously leads to a deleterious effect on affordability. A decrease in mortgage applications may also suggest that would-be buyers are dropping out of the market as they are unable to locate affordable homes. This lack of affordability affects not only first-time buyers but also existing homeowners, who may abandon the idea of trading up to a larger property at this time.

There is, of course, a risk of buyers with minimal equity getting into difficulty should interest rates rise. Buyers need a minimum of 10 percent equity just to cover selling costs and not be ‘under water’ with their mortgage. According to Stessa.com, less than 4 percent of buyers nationwide are in this perilous situation; however, this percentage varies considerably in different parts of the country, as shown in this blog post. In Louisiana, for example, the percentage of owners with less than 10 percent equity is a whopping 10.7 percent, the highest in the nation; at the other end of the scale, Oregon has only 2 percent of homeowners with this low level of equity. A sharp rise in interest rates in the future could trigger a number of distressed sales; nonetheless, it is debatable whether the relatively small percentage of affected owners would have a huge impact on prices nationwide.

It would have been understandable if we had experienced a decrease in house prices during and after a pandemic, given that many people were laid off or furloughed. Families living through lockdowns would be less likely to move, or at least more likely to postpone moving, while those finding themselves suddenly without income – or with reduced income – might decide to sell. In fact, it is glaringly obvious that the exact opposite has happened due to other aforementioned factors: low inventory, combined with low-interest rates that are keeping mortgages affordable. A fear of missing out may be spurring renters into making the decision to buy, and current owners to upgrade, especially if they need extra space to work from home. Seasonal changes may bring a slowdown over the fall and winter but it seems likely that the current seller’s market will continue for a while yet, and that both sales and prices will continue to rise.